Future prospects of the Company

The Company proposes to diversify into the business of Sugar manufacturing and construction activities and the growth of the both are linked to GDP growth of the Country.

India’s GDP maintained its steady rise in 2007-08 to clock 9% growth. The average GDP for four years upto 2007-08 had been 8.6%, signifying stable economic growth and domestic demand. Although, because of global slowdown, sub-prime issues, high interest rate factors the GDP growth of Indian Economy was adversely effected in the year 2008-09, the growth momentum is since resumed because of high domestic consumptions, corrective steps from time to time taken by the Indian Government and RBI for boosting consumptions and demands. The Government of India as well as analysts all over world targets a higher GDP growth of the Indian Economy, irrespective of the world trend.

This consistent growth of the economy has catapulted India as the fastest growing economy after China for the following reasons:

- Changing composition of GDP; reduced dependence on agriculture and growing industrial and services sectors

- Strong outsourcing growth momentum – IT and financial services, healthcare and manufacturing

- Strong improvement in the external sector and a gradual fiscal deficit correction

Sugar

Sugar is one of the essential items not only in the household sector but also in various industrial formulations in pharmaceutical sector, confectionery, soft drinks, sweets etc. The consumption of sugar in the country is on the increase due to population growth as also due to various development plans of the Government. Still the per capita sugar consumption in India is much lower than the world standard and even from the developing countries. However, the per capita consumption of sugar is on the increase on account of improved standard of living and the changing life style of rural masses which now prefers sugar than any other alternate sweetening material.

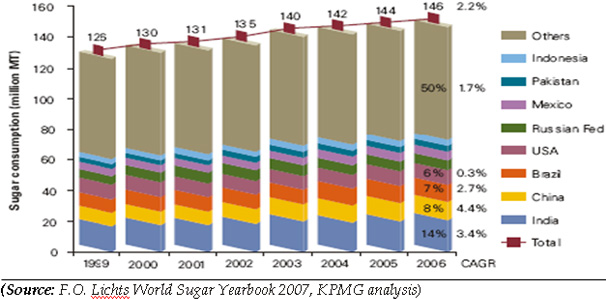

The total world consumption is at around 146 million MT of sugar. India is the largest consumer of sugar followed by China, Brazil, USA and the Russian federation. Consumption in China, India and Brazil is growing at a higher rate than the world average of 2.2 percent. Consequently, these geographies are expected to play a larger role in the global sugar trade in the coming years.

The Indian sugar consumption has steadily increased at 3.5 percent since 1996. Typically, sugar consumption is driven by the GDP growth and this has been the case for India as well. The per capita consumption has seen a steady growth of 2.1 percent CAGR over this period, while the population has grown at a CAGR of 1.4 percent.

Global Sugar Industry

The world sugar economy is facing a second consecutive year of a significant gap between world consumption and production. The first revision of the world sugar balance for October 2009 to September 2010 puts world production at 159.887 mln tonnes, raw value, up by 6.911 mln tonnes or 4.5% from the last season. A forecasted limited growth in sugar output in Brazil, a modest production recovery in India after last season’s unprecedented shortfall, and a higher sugar crop in the EU have become the three major supply features of 2009/10. World consumption is expected to grow at a rate significantly lower than the long-term 10 year average (1.71% and 2.66%, respectively). The lower growth is attributed to impacts of the 2008/09 global recession on sugar consumption growth rates in developing countries as well as soaring world market prices. Even so, global use of sugar is expected to reach 167.134 mln tonnes. Therefore, the growth in global production is far too small to cover sugar consumption and the world statistical deficit is expected to reach 7.247 mln tonnes as against 8.404 mln tonnes projected in September, 2009.

A summary of the revised world sugar balance in 2009/10 is provided in the table below.

World Sugar Balance

|

|||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||

| Source: ISO quarterly market outlook, November 2009 |

Indian Sugar Industry

Indian sugar industry has entered the strongest up cycle (lowest stock to use ratio) in the history of 50 years after witnessing supply glut in previous two sugar seasons in a row (SS 2006-08). In SS2006-07, sugar production reached all-time high of 28.3 mn tonnes, registering a growth of 46.6% on yoy basis and it declined marginally by 7.1% to 26.3 mn tonnes in SS2007-08. Sugar production reached an all-time low of 14.7 mn tonnes during SS2008-09 due to sharp fall in the sugarcane acreage. However, sugar consumption continued to grow at a steady pace. It grew at a CAGR of 4% during SS 07-09.

In SS2008-09, on account of a steep fall in sugar production and fall in the stock to use ratio, the average wholesale prices increased by almost 50% on yoy basis. This had a positive impact on the margins of sugar companies in the Q4FY09.

Deficit situation in India to continue in SS2009-10 and SS2010-11. We believe that India will bridge the gap between demand and supply through imports.

Production, Consumptiion and Yield position in India [In million tones]

|

|||||||||||||||||||||||||

|

|||||||||||||||||||||||||

| Source : Industry Data [Weekender, KRC Research – Feb 6th, 2010] |

Sugar Outlook

The 2008-2009 Sugar Season was the first year of upturn in the sugar cycle, after two years (2006-2007 and 2007-2008 Sugar Seasons) of surplus production and rising sugar inventories.

Sugar mill delivery prices have risen by nearly 100% over a year ago, and are up nearly 40% since October. In the 2009-10 sugar marketing season (Oct-Sep), India’s sugar production is estimated to improve a bit over the previous year’s level of 15 million tonnes (mt), but still fall short of the 23 mt needed to meet domestic consumption. The International Sugar Organisation has estimated sugar production to increase by 4.5% to about 160 mt, about 7 mt short of demand. The full effect of this deficit is being felt on sugar prices.

Co- Generation

We will produce electricity for our sugar mill operations. We propose to generate electric power mainly through the burning of bagasse, a primary by-product of our sugar production process. Bagasse is a combustible material which when burned produces steam, which in turn is used to generate electric power. We propose establishment of co-generation facilities at the Sugar Mill with a capacity of 25 MW per hour.

Co-generation is the concept of simultaneously producing two forms of energy. One of the forms of energy must always be heat and the other may be electricity or mechanical energy. In a conventional power plant, fuel is burnt in a boiler to generate steam. This steam is used to drive a turbine, which in turn drives an alternator to produce electric power. The exhaust steam is generally condensed to water, which goes back to the boiler. However, in a co-generation plant, some amount of steam may be extracted from the turbine at the required pressure and temperature for use in the manufacturing process. The power produced by co-generation is used in

internal industry processes, and excess power is sold to State Utilities/ Distribution Companies. The realization from the exportable power is dependent on the long term power purchase agreements with government and power companies. Cogeneration also has proven revenue potential in Clean Development Mechanism (CDM) based carbon credits. The present exportable power generated by the sugar industry is 847 MW, but this could increase to approximately 9,700 MW by 2017. Cogeneration can enable India to meet the goals for “green energy” from renewable and sustainable biomass. Cogeneration can be a small, but certain step to bridge the availability gap for power. Consistent policy would be needed to encourage investments in cogeneration capacities.

Benefits of Co-generation Systems:

- Provides economic competitive advantages through a maximized return on investment by utilizing the same fuel to provide heat and electricity;

- Environment friendly because of reduced air emissions of Green House Gases, sulphur dioxide, nitrogen oxides, and particulate matters;

- A reliable source of power and process steam or heat;

- Onsite electricity generation can reduce transmission and distribution losses; and

- Low gestation period.

COMPETITIVE STRENGTHS

Our primary competitive strengths include the following:

- Our operations are strategically located within the largest domestic market for sugar.

Our operations will be ocated in India, the largest market for sugar in the world in terms of consumer demand for refined sugar. The sugar mill is located at Motihari, the district headquarter of East Champaran, Bihar on a plot of land measuring 195 Bighas, 18 Cottahs. The site is 3 km from Motihari railway station. The Sugar mill is served with a railway siding. Motihari is connected with National Highway no 28 which is very convenient for transportation of incoming raw material, sugar product, crystal sugar and byproduct - molasses. The Sugar mill is located in the heart of the sugar cane belt of Bihar and hence supply of sugar cane for crushing is assured. - We have strong relationships with sugarcane farmers.

We believe in making timely payments to sugarcane farmers and therefore are confident to built strong relationships and goodwill with them which is an important factor in our industry. Despite the cyclical nature of the sugar industry, we have strong ties with the desired sugarcane growers. We believe that these relationships are a competitive advantage as farmers have no obligation to grow sugarcane and may from time to time switch to crops that may be more profitable. However, we believe that paying farmers on a timely basis provides an incentive for farmers to continue cultivating sugarcane. - High recovery rates.

We are confident to achieve relatively high recovery rates of sugar from sugarcane, which is the key profit driver for any sugar mill. We believe our cost of converting sugarcane into sugar will be very competitive in the industry due to the large scale of our operations and continuous addition of balancing equipments for repairs, maintenance, modernization and information technology. Our proposed information technology system will assists us in achieving higher operational efficiencies. We will have an electronic database which helps us to plan and manage our procurement of sugarcane from farmers and to monitor various activities, including scheduling sugarcane deliveries from farmers, payment to sugarcane farmers and developmental activities in our reserved areas. - We will adopt an integrated business model to balance the cyclical effects of the sugar business.

In order to mitigate the effects of downward price cycles in the Indian sugar industry which typically last three to four years, we propose to adopt a business model that integrates the sugar manufacturing process with the production of a diverse array of products. In addition, we proposes to generate power and sell excess power that we generate from the bagasse produced by our sugar operations. - Cordial Human relationship.

The Labour –Management relations at the factory are very cordial. We propose to settle all dues of our workers/employees and also rationalization of the existing workforce followed by appointment of the need-based workers and employees in due course preferably from the nearby areas. We formulate our Human Resource policies after discussions with employees across departments and locations. The policies cover our objectives, eligibility and coverage, policy and procedures. We review, revise and update our human resources policies from time to time to make them relevant, effective and useful to the employees as well as to us. - We have an elaborate sugarcane collection network.

In order to carry out cane development and cane procurement activities effectively and smoothly, we will have a dedicated cane department to control and supervise the cane development and procurement activities. We will purchase sugarcane directly from the farmers without involvement of any intermediaries. Based on the age of the crop, variety and maturity, a harvesting program is proposed to be chalked out for desired quantity and quality of cane to be procured on a day-to-day basis. The Cane Managers will issue cutting orders / harvesting permits based on date-wise cum pre-harvesting maturity survey. Accordingly cane transporting vehicles along with harvesting groups are allotted for harvesting and transporting cane to the mill. - Committed and experienced management team

Mr. B. K. Nopany, the Chairman cum Managing Director is recognized for his expertise and involvement in the sugar industry in India.

He is highly committed to our business and forward looking. Mr. Nopany pioneered the strategy of acquiring and putting to use leased assets for sugar manufacturing from the loss making company at very low costs. This will help our Company to scale up our operations within a short span of time. - Increase our focus on corporate and high-value customers

We intend to be the “supplier of choice” for our industrial buyers.

We are actively looking to enhance our presence within industrial buyers in the FMCG sector by continually upgrading our processes and quality systems. We supply our product to the corporate players in the FMCG sector. - To reduce price risk in sugar by hedging

We intend to use our large trade flow, which consists of our sales of manufactured and traded sugar to manage price risk.

We will actively utilize NCDEX and international commodity exchanges to fix the prices of our sugar for forward sales. The percentage of forward cover is decided by our internal risk management team and is driven by our perception of trends in the market. This hedging strategy provides us a protection to the price volatility in commodity market and stable revenue flows. - State-of-art Technology and sound financial planning

The sugar industry in India is highly fragmented with manufacturers having limited pricing power.

However, we believe that because of state-of-art technology, ongoing pursuit of a diverse product line based on an integrated business model, along with sound financial planning will provide us with the ability to perform optimally during all phases of the sugar business cycle. - We plan to capitalize on future upward pricing trends in the sugar cycle based on the large crushing capacity of our sugar mills.

We propose to expand our sugarcane crushing capacity in the near future. As a result of this expansion, we believe that our ability to produce such a high volume of sugar puts us in an advantageous position to benefit from any upward price trend in the Indian sugar cycle. In addition, to take advantage of reduced tariffs on sugar imports and to fully capitalize on an expected increase in sugar prices over the next few years, we plan to import raw sugar in the coming seasons. - We plan to diversify our products and increasing the production of value-added products.

We plan to increasingly adding value to the by-products of our sugar manufacturing process to diversify our product line, realize higher revenue from our sugar processing operations and mitigate the effects of over reliance on sugar sales, particularly during downward price trends and seasonal variations in the Indian sugar industry. Our have plan for diversified product line, which will consist of industrial alcohol, particle board and medium-density fibre board.

Construction

The Company also proposes to diversify into the business of construction and selling of residential houses. Mr. B. K. Nopany, the Chairman cum Managing Director of the Company has long-term experience of real estate development. The proposed construction activities are proposed to be financed entirely either out of internal resources or advance from customers.

The Indian construction industry is an integral part of the Indian economy and an important portion of investments into the development of the Indian Economy takes place through the construction industry. The construction industry is expected to grow with further economic development, industrialisation, urbanisation and improvements in the standard of living.

According to Indian Infrastructure, the Indian construction industry accounts for more than 5% of India’s GDP and is the second largest employer after agriculture, employing nearly 32 million people. In the course of liberalization of the Indian economy, the Government has placed a priority on infrastructure development and emphasised the involvement of private capital and management in order to respond to the growing demand for new infrastructure projects.

According to the Indian Central Statistical Organisation, investments in construction in India grew at a compounded annual growth rate of 12% during the last ten years.

According to Indian Infrastructure, the Indian construction industry accounts for more than 5% of India’s GDP and is the second largest employer after agriculture, employing nearly 32 million people. In the course of liberalization of the Indian economy, the Government has placed a priority on infrastructure development and emphasised the involvement of private capital and management in order to respond to the growing demand for new infrastructure projects.

According to the Indian Central Statistical Organisation, investments in construction in India grew at a compounded annual growth rate of 12% during the last ten years.

Construction spending for urban infrastructure is expected to amount to Rs. 827 bn (US$ 18.8 bn) i.e. 23% of the total construction spending in the Eleventh Five Year Plan. The key drivers include a growing Indian industry and economy, increasing urbanisation and household growth. The mounting demand for building and housing construction is due to the strong growth in the industrial, manufacturing and real estate sectors.

Affordable Housing

As mentioned above, in spite of the recent economic slowdown, India is expected to remain amongst the fastest growing economies of the world, leading to a significant increase in purchasing power of its population. As per a study conducted by Mckinsey Global Institute, the percentage of Middle Income Group (MIG) households is likely to increase from 6 per cent. in 2005 to 24 per cent. in 2015 and 45 per cent. In 2025.

|

||||||||||||||||

|

||||||||||||||||

| (Source: Mckinsey Global Institute) |

As per the Ministry of Housing and Urban Poverty Alleviation (MHUPA), there was a shortage of 24.71 million dwelling units for 67.4 million households in India in 2007. Out of this, close to 99 per cent. of shortage is in the Economically Weaker Section (EWS) and LIG (Low Income Group) segment. Housing shortage is expected to increase to 26.53 million dwelling units for 75.01 million households by 2012, of which approximately 85 per cent. is expected to be in the EWS and LIG segment.

|

||||||||

|

||||||||

| (Source: Ministry of Housing and Urban Poverty Alleviation, India) |

Ministry of Housing and Urban Poverty Alleviation, India (MHUPA) has framed the National Urban Housing and Habitat Policy, which carefully analyses ways and means of providing ‘Affordable Housing to All’ with special emphasis on the EWS and LIG segments. The new policy lays emphasis on earmarking of land for the EWS/LIG groups in new housing projects and also emphasizes on the Government retaining its role in social housing so that affordable housing is made available to EWS and LIG of the population as they lack affordability and are hopelessly out priced in urban land markets.

Government initiatives coupled with increasing per capita income in India on the back of high economic growth is expected to provide strong impetus to affordable housing demand.

COMPETITIVE STRENGTHS

Our primary competitive strengths in respect of construction activities include the following:

- Increased focus on the Affordable Housing segment.

We will give thrust on launching Affordable Housing a segment which we believe is relatively less affected by the recent economic downturn. Within the Affordable Housing segment, we intend to concentrate on offering such projects with a price ranging between Rs. 1.40 million to Rs. 3.0 million. We believe that there is a growth potential in the Affordable Housing segment as the demand for such properties may increase with the growth in the Indian economy and the corresponding increase in urbanization, together with the attractive financing options available in this segment. We believe that our operational and execution capabilities will enable us to effectively compete in this segment of the housing market. - Strengthen financial resources.

Our strengthened financial resources including by way of internal accruals will enable us to undertake construction activities without any hindrance and ensure timely completion of the projects apart from facilitating economical purchases of construction materials apart from land, which will lead to a high reputation. - Experienced management and employees.

Our management team has significant experience in the real estate sector and our staff of professionals cover a variety of disciplines, including architecture, engineering, project supervision, accounting, marketing and sales. Our management and professional personnel have extensive experience in anticipating market trends, identifying new markets and potential sites for development and acquiring land and development rights, as well as in the design, engineering, construction, supervision and marketing of projects. Their experience includes relationships with the suppliers from whom we source construction materials and the contractors we engage for construction services, allowing us to better manage the quality, schedule and cost of the materials and construction in our projects. In order to expedite the decision making process and to facilitate speedy implementation of the real estate projects, we have adopted a model in which critical functions like project planning, procurement and project monitoring are managed from our corporate office and key support functions such as obtaining regulatory approvals, pre-marketing and marketing are the responsibility of our representatives at the State and local level. This model enables us to maintain a balance between the customization of our projects to cater to the demographics of a location while maintaining our standards of quality and efficiency.